.png)

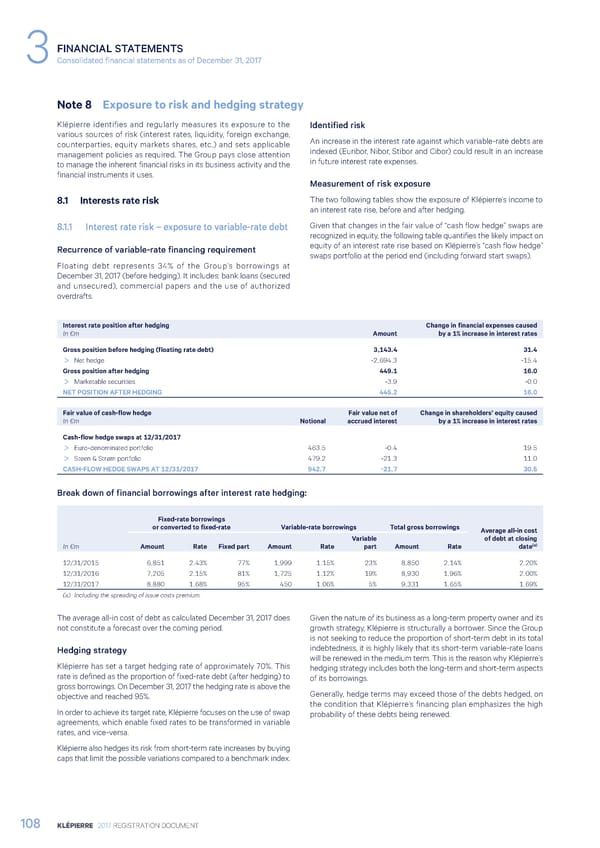

FINANCIAL STATEMENTS 3Consolidated financial statements as of December 31, 2017 Note 8 Exposure to risk and hedging strategy Klépierre identifies and regularly measures its exposure to the Identified risk various sources of risk (interest rates, liquidity, foreign exchange, An increase in the interest rate against which variable-rate debts are counterparties, equity markets shares, etc.) and sets applicable indexed (Euribor, Nibor, Stibor and Cibor) could result in an increase management policies as required. The Group pays close attention in future interest rate expenses. to manage the inherent financial risks in its business activity and the financial instruments it uses. Measurement of risk exposure 8.1 Interests rate risk The two following tables show the exposure of Klépierre’s income to an interest rate rise, before and after hedging. 8.1.1 Interest rate risk – exposure to variable-rate debt Given that changes in the fair value of “cash flow hedge” swaps are recognized in equity, the following table quantifies the likely impact on Recurrence of variable-rate financing requirement equity of an interest rate rise based on Klépierre’s “cash flow hedge” swaps portfolio at the period end (including forward start swaps). Floating debt represents 34% of the Group’s borrowings at December 31, 2017 (before hedging). It includes: bank loans (secured and unsecured), commercial papers and the use of authorized overdrafts. Interest rate position after hedging Change in financial expenses caused In €m Amount by a 1% increase in interest rates Gross position before hedging (floating rate debt) 3,143.4 31.4 > Net hedge -2,694.3 -15.4 Gross position after hedging 449.1 16.0 > Marketable securities -3.9 -0.0 NET POSITION AFTER HEDGING 445.2 16.0 Fair value of cash-flow hedge Fair value net of Change in shareholders’ equity caused In €m Notional accrued interest by a 1% increase in interest rates Cash-flow hedge swaps at 12/31/2017 > Euro-denominated portfolio 463.5 -0.4 19.5 > Steen & Strøm portfolio 479.2 -21.3 11.0 CASH-FLOW HEDGE SWAPS AT 12/31/2017 942.7 -21.7 30.5 Break down of financial borrowings after interest rate hedging: Fixed-rate borrowings or converted to fixed-rate Variable-rate borrowings Total gross borrowings Average all-in cost Variable of debt at closing In €m Amount Rate Fixed part Amount Rate part Amount Rate date(a) 12/31/2015 6,851 2.43% 77% 1,999 1.15% 23% 8,850 2.14% 2.20% 12/31/2016 7,205 2.15% 81% 1,725 1.12% 19% 8,930 1.96% 2.00% 12/31/2017 8,880 1.68% 95% 450 1.06% 5% 9,331 1.65% 1.69% (a) Including the spreading of issue costs premium. The average all-in cost of debt as calculated December 31, 2017 does Given the nature of its business as a long-term property owner and its not constitute a forecast over the coming period. growth strategy, Klépierre is structurally a borrower. Since the Group is not seeking to reduce the proportion of short-term debt in its total Hedging strategy indebtedness, it is highly likely that its short-term variable-rate loans will be renewed in the medium term. This is the reason why Klépierre’s Klépierre has set a target hedging rate of approximately 70%. This hedging strategy includes both the long-term and short-term aspects rate is defined as the proportion of fixed-rate debt (after hedging) to of its borrowings. gross borrowings. On December 31, 2017 the hedging rate is above the objective and reached 95%. Generally, hedge terms may exceed those of the debts hedged, on the condition that Klépierre’s financing plan emphasizes the high In order to achieve its target rate, Klépierre focuses on the use of swap probability of these debts being renewed. agreements, which enable fixed rates to be transformed in variable rates, and vice-versa. Klépierre also hedges its risk from short-term rate increases by buying caps that limit the possible variations compared to a benchmark index. 108 KLÉPIERRE 2017 REGISTRATION DOCUMENT

Registration Document 2017 Page 109 Page 111

Registration Document 2017 Page 109 Page 111