.png)

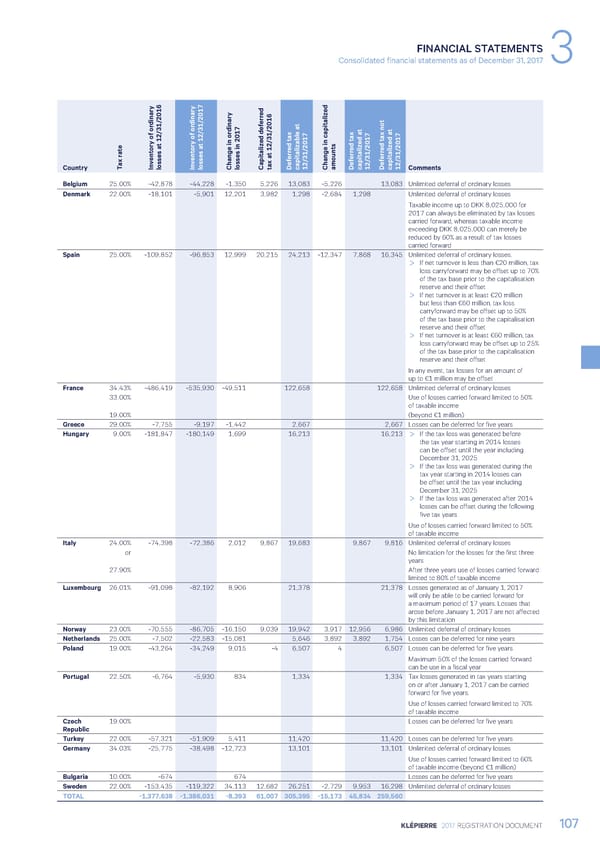

FINANCIAL STATEMENTS Consolidated financial statements as of December 31, 2017 3 d d e e dinary dinary err t aliz dinary t t d def ax ax d a ax not d a t 12/31/2016t 12/31/2017 e d table a s d te d te ate ory of ors aory of ors a s in 2017alizt 12/31/2016ealiz e aliz e aliz r ent ent err err err x v sse v sse sse ef ef ef a ax a Country T In lo In lo Change in orloCapittDcapit12/31/2017Change in capitamountDcapit12/31/2017Dcapit12/31/2017Comments Belgium 25.00% -42,878 -44,228 -1,350 5,226 13,083 -5,226 13,083 Unlimited deferral of ordinary losses Denmark 22.00% -18,101 -5,901 12,201 3,982 1,298 -2,684 1,298 Unlimited deferral of ordinary losses Taxable income up to DKK 8,025,000 for 2017 can always be eliminated by tax losses carried forward, whereas taxable income exceeding DKK 8,025,000 can merely be reduced by 60% as a result of tax losses carried forward Spain 25.00% -109,852 -96,853 12,999 20,215 24,213 -12,347 7,868 16,345 Unlimited deferral of ordinary losses. > If net turnover is less than €20 million, tax loss carryforward may be offset up to 70% of the tax base prior to the capitalisation reserve and their offset > If net turnover is at least €20 million but less than €60 million, tax loss carryforward may be offset up to 50% of the tax base prior to the capitalisation reserve and their offset > If net turnover is at least €60 million, tax loss carryforward may be offset up to 25% of the tax base prior to the capitalisation reserve and their offset In any event, tax losses for an amount of up to €1 million may be offset France 34.43% -486,419 -535,930 -49,511 122,658 122,658 Unlimited deferral of ordinary losses 33.00% Use of losses carried forward limited to 50% of taxable income 19.00% (beyond €1 million) Greece 29.00% -7,755 -9,197 -1,442 2,667 2,667 Losses can be deferred for five years Hungary 9.00% -181,847 -180,149 1,699 16,213 16,213 > If the tax loss was generated before the tax year starting in 2014 losses can be offset until the year including December 31, 2025 > If the tax loss was generated during the tax year starting in 2014 losses can be offset until the tax year including December 31, 2025 > If the tax loss was generated after 2014 losses can be offset during the following five tax years Use of losses carried forward limited to 50% of taxable income Italy 24.00% -74,398 -72,386 2,012 9,867 19,683 9,867 9,816 Unlimited deferral of ordinary losses or No limitation for the losses for the first three years 27.90% After three years use of losses carried forward limited to 80% of taxable income Luxembourg 26.01% -91,098 -82,192 8,906 21,378 21,378 Losses generated as of January 1, 2017 will only be able to be carried forward for a maximum period of 17 years. Losses that arose before January 1, 2017 are not affected by this limitation Norway 23.00% -70,555 -86,705 -16,150 9,039 19,942 3,917 12,956 6,986 Unlimited deferral of ordinary losses Netherlands 25.00% -7,502 -22,583 -15,081 5,646 3,892 3,892 1,754 Losses can be deferred for nine years Poland 19.00% -43,264 -34,249 9,015 -4 6,507 4 6,507 Losses can be deferred for five years Maximum 50% of the losses carried forward can be use in a fiscal year Portugal 22.50% -6,764 -5,930 834 1,334 1,334 Tax losses generated in tax years starting on or after January 1, 2017 can be carried forward for five years. Use of losses carried forward limited to 70% of taxable income Czech 19.00% Losses can be deferred for five years Republic Turkey 22.00% -57,321 -51,909 5,411 11,420 11,420 Losses can be deferred for five years Germany 34.03% -25,775 -38,498 -12,723 13,101 13,101 Unlimited deferral of ordinary losses Use of losses carried forward limited to 60% of taxable income (beyond €1 million) Bulgaria 10.00% -674 674 Losses can be deferred for five years Sweden 22.00% -153,435 -119,322 34,113 12,682 26,251 -2,729 9,953 16,298 Unlimited deferral of ordinary losses TOTAL -1,377,638 -1,386,031 -8,393 61,007 305,395 -15,173 45,834 259,560 KLÉPIERRE 2017 REGISTRATION DOCUMENT 107

Registration Document 2017 Page 108 Page 110

Registration Document 2017 Page 108 Page 110