.png)

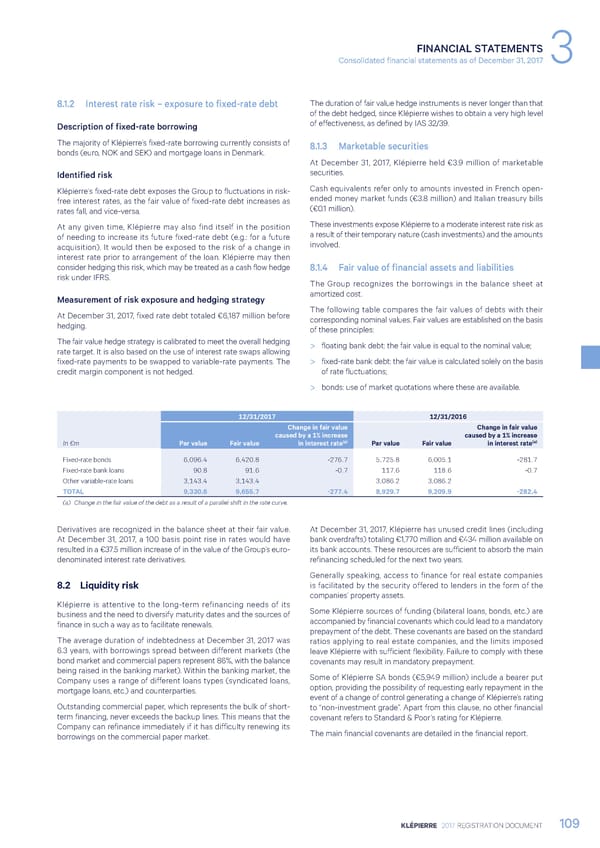

FINANCIAL STATEMENTS Consolidated financial statements as of December 31, 2017 3 8.1.2 Interest rate risk – exposure to fixed-rate debt The duration of fair value hedge instruments is never longer than that of the debt hedged, since Klépierre wishes to obtain a very high level Description of fixed-rate borrowing of effectiveness, as defined by IAS 32/39. The majority of Klépierre’s fixed-rate borrowing currently consists of 8.1.3 Marketable securities bonds (euro, NOK and SEK) and mortgage loans in Denmark. At December 31, 2017, Klépierre held €3.9 million of marketable Identified risk securities. Klépierre’s fixed-rate debt exposes the Group to fluctuations in risk- Cash equivalents refer only to amounts invested in French open- free interest rates, as the fair value of fixed-rate debt increases as ended money market funds (€3.8 million) and Italian treasury bills rates fall, and vice-versa. (€0.1 million). At any given time, Klépierre may also find itself in the position These investments expose Klépierre to a moderate interest rate risk as of needing to increase its future fixed-rate debt (e.g.: for a future a result of their temporary nature (cash investments) and the amounts acquisition). It would then be exposed to the risk of a change in involved. interest rate prior to arrangement of the loan. Klépierre may then consider hedging this risk, which may be treated as a cash flow hedge 8.1.4 Fair value of financial assets and liabilities risk under IFRS. The Group recognizes the borrowings in the balance sheet at Measurement of risk exposure and hedging strategy amortized cost. At December 31, 2017, fixed rate debt totaled €6,187 million before The following table compares the fair values of debts with their hedging. corresponding nominal values. Fair values are established on the basis of these principles: The fair value hedge strategy is calibrated to meet the overall hedging > floating bank debt: the fair value is equal to the nominal value; rate target. It is also based on the use of interest rate swaps allowing fixed-rate payments to be swapped to variable-rate payments. The > fixed-rate bank debt: the fair value is calculated solely on the basis credit margin component is not hedged. of rate fluctuations; > bonds: use of market quotations where these are available. 12/31/2017 12/31/2016 Change in fair value Change in fair value caused by a 1% increase caused by a 1% increase In €m Par value Fair value (a) Par value Fair value (a) in interest rate in interest rate Fixed-rate bonds 6,096.4 6,420.8 -276.7 5,725.8 6,005.1 -281.7 Fixed-rate bank loans 90.8 91.6 -0.7 117.6 118.6 -0.7 Other variable-rate loans 3,143.4 3,143.4 3,086.2 3,086.2 TOTAL 9,330.6 9,655.7 -277.4 8,929.7 9,209.9 -282.4 (a) Change in the fair value of the debt as a result of a parallel shift in the rate curve. Derivatives are recognized in the balance sheet at their fair value. At December 31, 2017, Klépierre has unused credit lines (including At December 31, 2017, a 100 basis point rise in rates would have bank overdrafts) totaling €1,770 million and €434 million available on resulted in a €37.5 million increase of in the value of the Group’s euro- its bank accounts. These resources are sufficient to absorb the main denominated interest rate derivatives. refinancing scheduled for the next two years. Generally speaking, access to finance for real estate companies 8.2 Liquidity risk is facilitated by the security offered to lenders in the form of the companies’ property assets. Klépierre is attentive to the long-term refinancing needs of its Some Klépierre sources of funding (bilateral loans, bonds, etc.) are business and the need to diversify maturity dates and the sources of accompanied by financial covenants which could lead to a mandatory finance in such a way as to facilitate renewals. prepayment of the debt. These covenants are based on the standard The average duration of indebtedness at December 31, 2017 was ratios applying to real estate companies, and the limits imposed 6.3 years, with borrowings spread between different markets (the leave Klépierre with sufficient flexibility. Failure to comply with these bond market and commercial papers represent 86%, with the balance covenants may result in mandatory prepayment. being raised in the banking market). Within the banking market, the Some of Klépierre SA bonds (€5,949 million) include a bearer put Company uses a range of different loans types (syndicated loans, option, providing the possibility of requesting early repayment in the mortgage loans, etc.) and counterparties. event of a change of control generating a change of Klépierre’s rating Outstanding commercial paper, which represents the bulk of short- to “non-investment grade”. Apart from this clause, no other financial term financing, never exceeds the backup lines. This means that the covenant refers to Standard & Poor’s rating for Klépierre. Company can refinance immediately if it has difficulty renewing its The main financial covenants are detailed in the financial report. borrowings on the commercial paper market. KLÉPIERRE 2017 REGISTRATION DOCUMENT 109

Registration Document 2017 Page 110 Page 112

Registration Document 2017 Page 110 Page 112