.png)

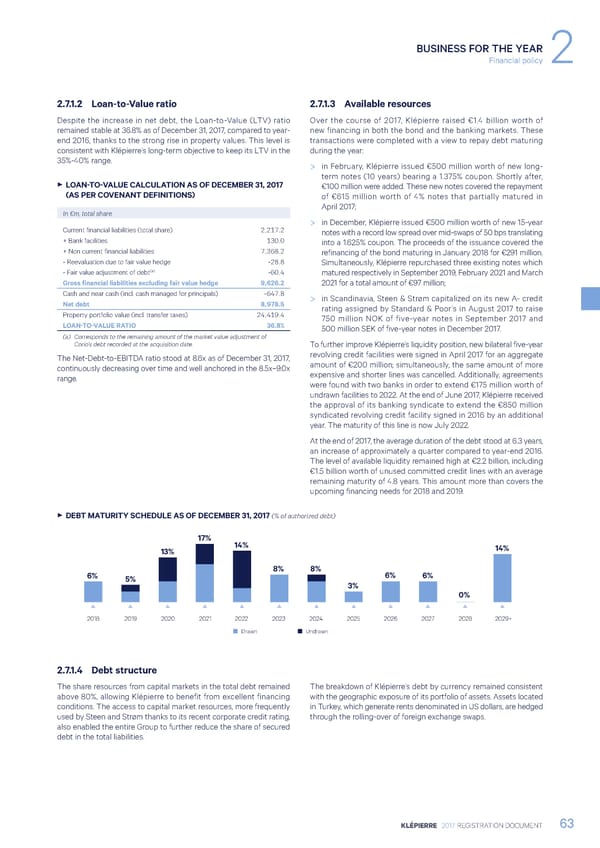

BUSINESS FOR THE YEAR Financial policy 2 2.7.1.2 Loan-to-Value ratio 2.7.1.3 Available resources Despite the increase in net debt, the Loan-to-Value (LTV) ratio Over the course of 2017, Klépierre raised €1.4 billion worth of remained stable at 36.8% as of December 31, 2017, compared to year- new financing in both the bond and the banking markets. These end 2016, thanks to the strong rise in property values. This level is transactions were completed with a view to repay debt maturing consistent with Klépierre’s long-term objective to keep its LTV in the during the year: 35%-40% range. > in February, Klépierre issued €500 million worth of new long- term notes (10 years) bearing a 1.375% coupon. Shortly after, 3 LOAN-TO-VALUE CALCULATION AS OF DECEMBER 31, 2017 €100 million were added. These new notes covered the repayment (AS PER COVENANT DEFINITIONS) of €615 million worth of 4% notes that partially matured in April 2017; In €m, total share > in December, Klépierre issued €500 million worth of new 15-year Current financial liabilities (total share) 2,217.2 notes with a record low spread over mid-swaps of 50 bps translating + Bank facilities 130.0 into a 1.625% coupon. The proceeds of the issuance covered the + Non current financial liabilities 7,368.2 refinancing of the bond maturing in January 2018 for €291 million. - Reevaluation due to fair value hedge -28.8 Simultaneously, Klépierre repurchased three existing notes which (a) -60.4 - Fair value adjustment of debt matured respectively in September 2019, February 2021 and March Gross financial liabilities excluding fair value hedge 9,626.2 2021 for a total amount of €97 million; Cash and near cash (incl. cash managed for principals) -647.8 > in Scandinavia, Steen & Strøm capitalized on its new A- credit Net debt 8,978.5 rating assigned by Standard & Poor’s in August 2017 to raise Property portfolio value (incl. transfer taxes) 24,419.4 750 million NOK of five-year notes in September 2017 and LOAN-TO-VALUE RATIO 36.8% 500 million SEK of five-year notes in December 2017. (a) Corresponds to the remaining amount of the market value adjustment of Corio’s debt recorded at the acquisition date. To further improve Klépierre’s liquidity position, new bilateral five-year The Net-Debt-to-EBITDA ratio stood at 8.6x as of December 31, 2017, revolving credit facilities were signed in April 2017 for an aggregate continuously decreasing over time and well anchored in the 8.5x–9.0x amount of €200 million; simultaneously, the same amount of more range. expensive and shorter lines was cancelled. Additionally, agreements were found with two banks in order to extend €175 million worth of undrawn facilities to 2022. At the end of June 2017, Klépierre received the approval of its banking syndicate to extend the €850 million syndicated revolving credit facility signed in 2016 by an additional year. The maturity of this line is now July 2022. At the end of 2017, the average duration of the debt stood at 6.3 years, an increase of approximately a quarter compared to year-end 2016. The level of available liquidity remained high at €2.2 billion, including €1.5 billion worth of unused committed credit lines with an average remaining maturity of 4.8 years. This amount more than covers the upcoming financing needs for 2018 and 2019. 3 DEBT MATURITY SCHEDULE AS OF DECEMBER 31, 2017 (% of authorized debt) 17% 14% 13% 14% 6% 8% 8% 6% 6% 5% 3% 0% 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029+ Drawn Undrawn 2.7.1.4 Debt structure The share resources from capital markets in the total debt remained The breakdown of Klépierre’s debt by currency remained consistent above 80%, allowing Klépierre to benefit from excellent financing with the geographic exposure of its portfolio of assets. Assets located conditions. The access to capital market resources, more frequently in Turkey, which generate rents denominated in US dollars, are hedged used by Steen and Strøm thanks to its recent corporate credit rating, through the rolling-over of foreign exchange swaps. also enabled the entire Group to further reduce the share of secured debt in the total liabilities. KLÉPIERRE 2017 REGISTRATION DOCUMENT 63

Registration Document 2017 Page 64 Page 66

Registration Document 2017 Page 64 Page 66