.png)

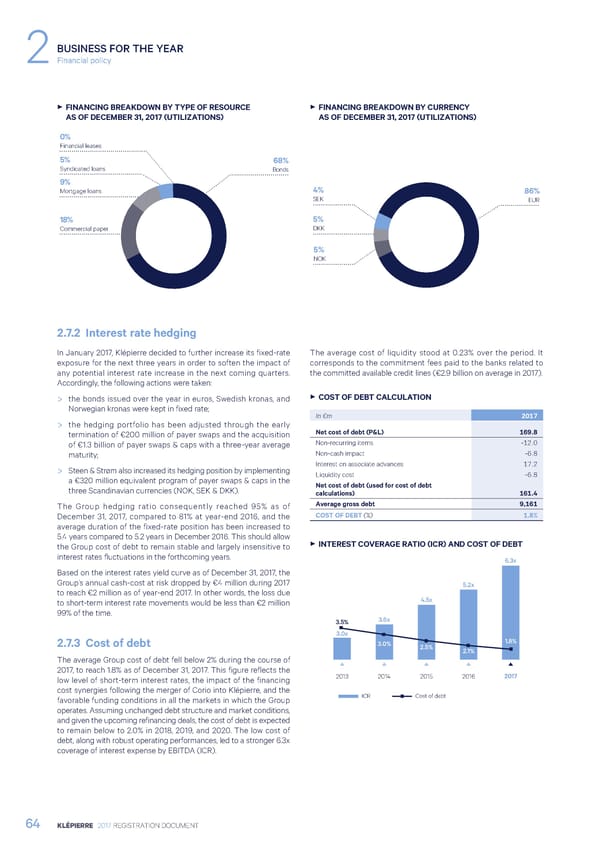

BUSINESS FOR THE YEAR 2Financial policy 3 FINANCING BREAKDOWN BY TYPE OF RESOURCE 3 FINANCING BREAKDOWN BY CURRENCY AS OF DECEMBER 31, 2017 (UTILIZATIONS) AS OF DECEMBER 31, 2017 (UTILIZATIONS) 0% Financial leases 5% 68% Syndicated loans Bonds 9% Mortgage loans 4% 86% SEK EUR 18% 5% Commercial paper DKK 5% NOK 2.7.2 Interest rate hedging In January 2017, Klépierre decided to further increase its fixed-rate The average cost of liquidity stood at 0.23% over the period. It exposure for the next three years in order to soften the impact of corresponds to the commitment fees paid to the banks related to any potential interest rate increase in the next coming quarters. the committed available credit lines (€2.9 billion on average in 2017). Accordingly, the following actions were taken: > the bonds issued over the year in euros, Swedish kronas, and 3 COST OF DEBT CALCULATION Norwegian kronas were kept in fixed rate; In €m 2017 > the hedging portfolio has been adjusted through the early termination of €200 million of payer swaps and the acquisition Net cost of debt (P&L) 169.8 of €1.3 billion of payer swaps & caps with a three-year average Non-recurring items -12.0 maturity; Non-cash impact -6.8 > Steen & Strøm also increased its hedging position by implementing Interest on associate advances 17.2 a €320 million equivalent program of payer swaps & caps in the Liquidity cost -6.8 three Scandinavian currencies (NOK, SEK & DKK). Net cost of debt (used for cost of debt calculations) 161.4 The Group hedging ratio consequently reached 95% as of Average gross debt 9,161 December 31, 2017, compared to 81% at year-end 2016, and the COST OF DEBT (%) 1.8% average duration of the fixed-rate position has been increased to 5.4 years compared to 5.2 years in December 2016. This should allow 3 INTEREST COVERAGE RATIO (ICR) AND COST OF DEBT the Group cost of debt to remain stable and largely insensitive to interest rates fluctuations in the forthcoming years. 6.3x Based on the interest rates yield curve as of December 31, 2017, the Group’s annual cash-cost at risk dropped by €4 million during 2017 5.2x to reach €2 million as of year-end 2017. In other words, the loss due to short-term interest rate movements would be less than €2 million 4.5x 99% of the time. 3.5% 3.6x 3.0x 2.7.3 Cost of debt 3.0% 1.8% 2.5% 2.1% The average Group cost of debt fell below 2% during the course of 2017, to reach 1.8% as of December 31, 2017. This figure reflects the 2017 low level of short-term interest rates, the impact of the financing 2013 2014 2015 2016 cost synergies following the merger of Corio into Klépierre, and the favorable funding conditions in all the markets in which the Group ICR Cost of debt operates. Assuming unchanged debt structure and market conditions, and given the upcoming refinancing deals, the cost of debt is expected to remain below to 2.0% in 2018, 2019, and 2020. The low cost of debt, along with robust operating performances, led to a stronger 6.3x coverage of interest expense by EBITDA (ICR). 64 KLÉPIERRE 2017 REGISTRATION DOCUMENT

Registration Document 2017 Page 65 Page 67

Registration Document 2017 Page 65 Page 67