.png)

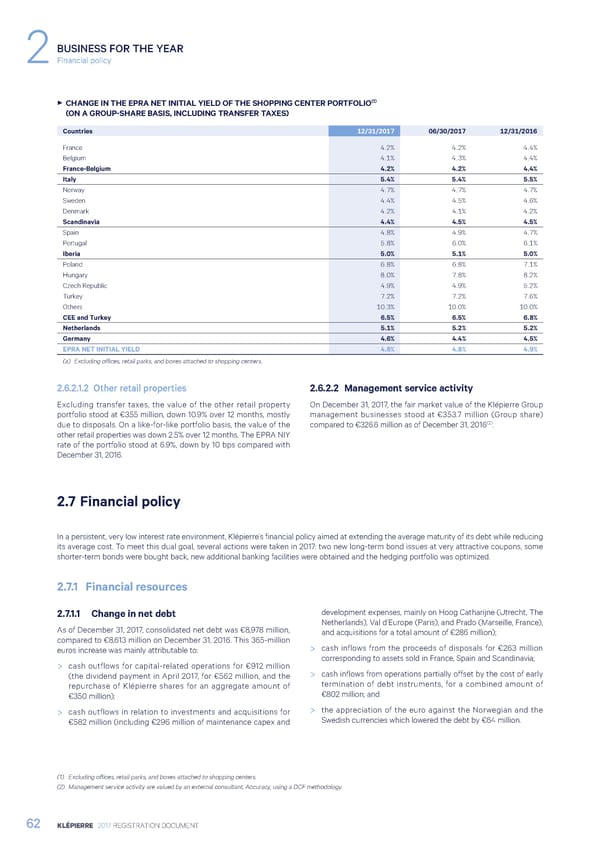

BUSINESS FOR THE YEAR 2Financial policy (1) 3 CHANGE IN THE EPRA NET INITIAL YIELD OF THE SHOPPING CENTER PORTFOLIO (ON A GROUP-SHARE BASIS, INCLUDING TRANSFER TAXES) Countries 12/31/2017 06/30/2017 12/31/2016 France 4.2% 4.2% 4.4% Belgium 4.1% 4.3% 4.4% France-Belgium 4.2% 4.2% 4.4% Italy 5.4% 5.4% 5.5% Norway 4.7% 4.7% 4.7% Sweden 4.4% 4.5% 4.6% Denmark 4.2% 4.1% 4.2% Scandinavia 4.4% 4.5% 4.5% Spain 4.8% 4.9% 4.7% Portugal 5.8% 6.0% 6.1% Iberia 5.0% 5.1% 5.0% Poland 6.8% 6.8% 7.1% Hungary 8.0% 7.8% 8.2% Czech Republic 4.9% 4.9% 5.2% Turkey 7.2% 7.2% 7.6% Others 10.3% 10.0% 10.0% CEE and Turkey 6.5% 6.5% 6.8% Netherlands 5.1% 5.2% 5.2% Germany 4.6% 4.4% 4.5% EPRA NET INITIAL YIELD 4.8% 4.8% 4.9% (a) Excluding offices, retail parks, and boxes attached to shopping centers. 2.6.2.1.2 Other retail properties 2.6.2.2 Management service activity Excluding transfer taxes, the value of the other retail property On December 31, 2017, the fair market value of the Klépierre Group portfolio stood at €355 million, down 10.9% over 12 months, mostly management businesses stood at €353.7 million (Group share) due to disposals. On a like-for-like portfolio basis, the value of the compared to €326.6 million as of December 31, 2016(2). other retail properties was down 2.5% over 12 months. The EPRA NIY rate of the portfolio stood at 6.9%, down by 10 bps compared with December 31, 2016. 2.7 Financial policy In a persistent, very low interest rate environment, Klépierre’s financial policy aimed at extending the average maturity of its debt while reducing its average cost. To meet this dual goal, several actions were taken in 2017: two new long-term bond issues at very attractive coupons, some shorter-term bonds were bought back, new additional banking facilities were obtained and the hedging portfolio was optimized. 2.7.1 Financial resources 2.7.1.1 Change in net debt development expenses, mainly on Hoog Catharijne (Utrecht, The Netherlands), Val d’Europe (Paris), and Prado (Marseille, France), As of December 31, 2017, consolidated net debt was €8,978 million, and acquisitions for a total amount of €286 million); compared to €8,613 million on December 31, 2016. This 365-million euros increase was mainly attributable to: > cash inflows from the proceeds of disposals for €263 million corresponding to assets sold in France, Spain and Scandinavia; > cash outflows for capital-related operations for €912 million (the dividend payment in April 2017, for €562 million, and the > cash inflows from operations partially offset by the cost of early repurchase of Klépierre shares for an aggregate amount of termination of debt instruments, for a combined amount of €350 million); €802 million; and > cash outflows in relation to investments and acquisitions for > the appreciation of the euro against the Norwegian and the €582 million (including €296 million of maintenance capex and Swedish currencies which lowered the debt by €64 million. (1) Excluding offices, retail parks, and boxes attached to shopping centers. (2) Management service activity are valued by an external consultant, Accuracy, using a DCF methodology. 62 KLÉPIERRE 2017 REGISTRATION DOCUMENT

Registration Document 2017 Page 63 Page 65

Registration Document 2017 Page 63 Page 65