.png)

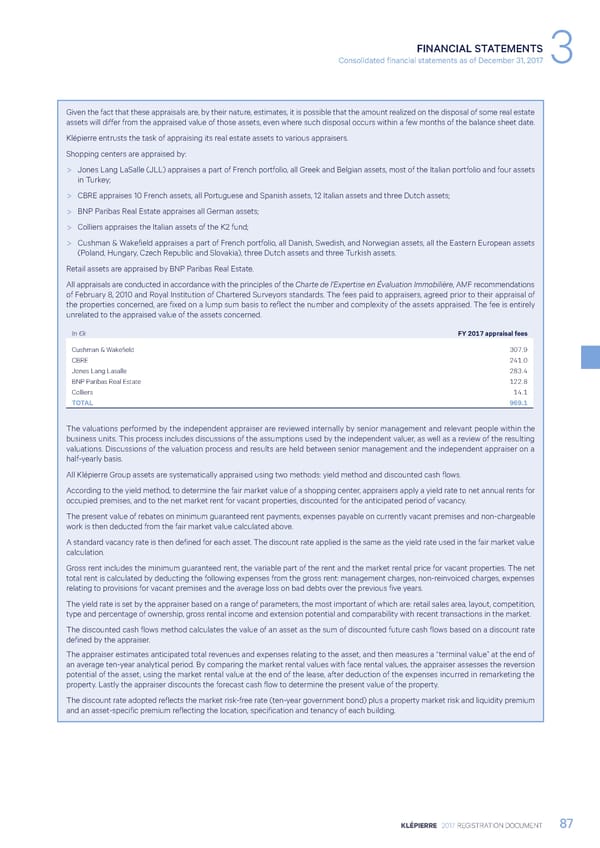

FINANCIAL STATEMENTS Consolidated financial statements as of December 31, 2017 3 Given the fact that these appraisals are, by their nature, estimates, it is possible that the amount realized on the disposal of some real estate assets will differ from the appraised value of those assets, even where such disposal occurs within a few months of the balance sheet date. Klépierre entrusts the task of appraising its real estate assets to various appraisers. Shopping centers are appraised by: > Jones Lang LaSalle (JLL) appraises a part of French portfolio, all Greek and Belgian assets, most of the Italian portfolio and four assets in Turkey; > CBRE appraises 10 French assets, all Portuguese and Spanish assets, 12 Italian assets and three Dutch assets; > BNP Paribas Real Estate appraises all German assets; > Colliers appraises the Italian assets of the K2 fund; > Cushman & Wakefield appraises a part of French portfolio, all Danish, Swedish, and Norwegian assets, all the Eastern European assets (Poland, Hungary, Czech Republic and Slovakia), three Dutch assets and three Turkish assets. Retail assets are appraised by BNP Paribas Real Estate. All appraisals are conducted in accordance with the principles of the Charte de l’Expertise en Évaluation Immobilière, AMF recommendations of February 8, 2010 and Royal Institution of Chartered Surveyors standards. The fees paid to appraisers, agreed prior to their appraisal of the properties concerned, are fixed on a lump sum basis to reflect the number and complexity of the assets appraised. The fee is entirely unrelated to the appraised value of the assets concerned. In €k FY 2017 appraisal fees Cushman & Wakefield 307.9 CBRE 241.0 Jones Lang Lasalle 283.4 BNP Paribas Real Estate 122.8 Colliers 14.1 TOTAL 969.1 The valuations performed by the independent appraiser are reviewed internally by senior management and relevant people within the business units. This process includes discussions of the assumptions used by the independent valuer, as well as a review of the resulting valuations. Discussions of the valuation process and results are held between senior management and the independent appraiser on a half-yearly basis. All Klépierre Group assets are systematically appraised using two methods: yield method and discounted cash flows. According to the yield method, to determine the fair market value of a shopping center, appraisers apply a yield rate to net annual rents for occupied premises, and to the net market rent for vacant properties, discounted for the anticipated period of vacancy. The present value of rebates on minimum guaranteed rent payments, expenses payable on currently vacant premises and non-chargeable work is then deducted from the fair market value calculated above. A standard vacancy rate is then defined for each asset. The discount rate applied is the same as the yield rate used in the fair market value calculation. Gross rent includes the minimum guaranteed rent, the variable part of the rent and the market rental price for vacant properties. The net total rent is calculated by deducting the following expenses from the gross rent: management charges, non-reinvoiced charges, expenses relating to provisions for vacant premises and the average loss on bad debts over the previous five years. The yield rate is set by the appraiser based on a range of parameters, the most important of which are: retail sales area, layout, competition, type and percentage of ownership, gross rental income and extension potential and comparability with recent transactions in the market. The discounted cash flows method calculates the value of an asset as the sum of discounted future cash flows based on a discount rate defined by the appraiser. The appraiser estimates anticipated total revenues and expenses relating to the asset, and then measures a “terminal value” at the end of an average ten-year analytical period. By comparing the market rental values with face rental values, the appraiser assesses the reversion potential of the asset, using the market rental value at the end of the lease, after deduction of the expenses incurred in remarketing the property. Lastly the appraiser discounts the forecast cash flow to determine the present value of the property. The discount rate adopted reflects the market risk-free rate (ten-year government bond) plus a property market risk and liquidity premium and an asset-specific premium reflecting the location, specification and tenancy of each building. KLÉPIERRE 2017 REGISTRATION DOCUMENT 87

Registration Document 2017 Page 88 Page 90

Registration Document 2017 Page 88 Page 90