.png)

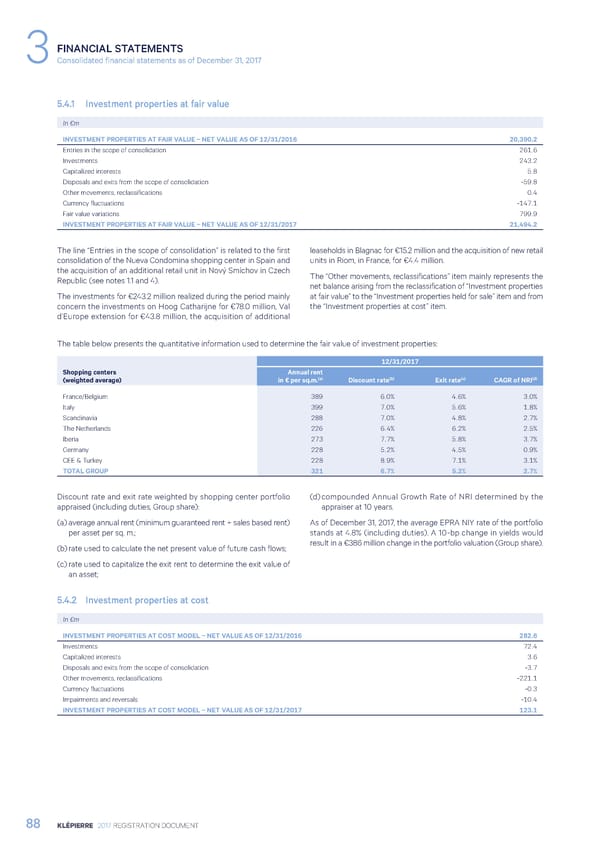

FINANCIAL STATEMENTS 3Consolidated financial statements as of December 31, 2017 5.4.1 Investment properties at fair value In €m INVESTMENT PROPERTIES AT FAIR VALUE – NET VALUE AS OF 12/31/2016 20,390.2 Entries in the scope of consolidation 261.6 Investments 243.2 Capitalized interests 5.8 Disposals and exits from the scope of consolidation -59.8 Other movements, reclassifications 0.4 Currency fluctuations -147.1 Fair value variations 799.9 INVESTMENT PROPERTIES AT FAIR VALUE – NET VALUE AS OF 12/31/2017 21,494.2 The line “Entries in the scope of consolidation” is related to the first leaseholds in Blagnac for €15.2 million and the acquisition of new retail consolidation of the Nueva Condomina shopping center in Spain and units in Riom, in France, for €4.4 million. the acquisition of an additional retail unit in Nový Smíchov in Czech The “Other movements, reclassifications” item mainly represents the Republic (see notes 1.1 and 4). net balance arising from the reclassification of “Investment properties The investments for €243.2 million realized during the period mainly at fair value” to the “Investment properties held for sale” item and from concern the investments on Hoog Catharijne for €78.0 million, Val the “Investment properties at cost” item. d’Europe extension for €43.8 million, the acquisition of additional The table below presents the quantitative information used to determine the fair value of investment properties: 12/31/2017 Shopping centers Annual rent (a) (b) (c) (d) (weighted average) in € per sq.m. Discount rate Exit rate CAGR of NRI France/Belgium 389 6.0% 4.6% 3.0% Italy 399 7.0% 5.6% 1.8% Scandinavia 288 7.0% 4.8% 2.7% The Netherlands 226 6.4% 6.2% 2.5% Iberia 273 7.7% 5.8% 3.7% Germany 228 5.2% 4.5% 0.9% CEE & Turkey 228 8.9% 7.1% 3.1% TOTAL GROUP 321 6.7% 5.2% 2.7% Discount rate and exit rate weighted by shopping center portfolio (d) compounded Annual Growth Rate of NRI determined by the appraised (including duties, Group share): appraiser at 10 years. (a) average annual rent (minimum guaranteed rent + sales based rent) As of December 31, 2017, the average EPRA NIY rate of the portfolio per asset per sq. m.; stands at 4.8% (including duties). A 10-bp change in yields would (b) rate used to calculate the net present value of future cash flows; result in a €386 million change in the portfolio valuation (Group share). (c) rate used to capitalize the exit rent to determine the exit value of an asset; 5.4.2 Investment properties at cost In €m INVESTMENT PROPERTIES AT COST MODEL – NET VALUE AS OF 12/31/2016 282.6 Investments 72.4 Capitalized interests 3.6 Disposals and exits from the scope of consolidation -3.7 Other movements, reclassifications -221.1 Currency fluctuations -0.3 Impairments and reversals -10.4 INVESTMENT PROPERTIES AT COST MODEL – NET VALUE AS OF 12/31/2017 123.1 88 KLÉPIERRE 2017 REGISTRATION DOCUMENT

Registration Document 2017 Page 89 Page 91

Registration Document 2017 Page 89 Page 91