.png)

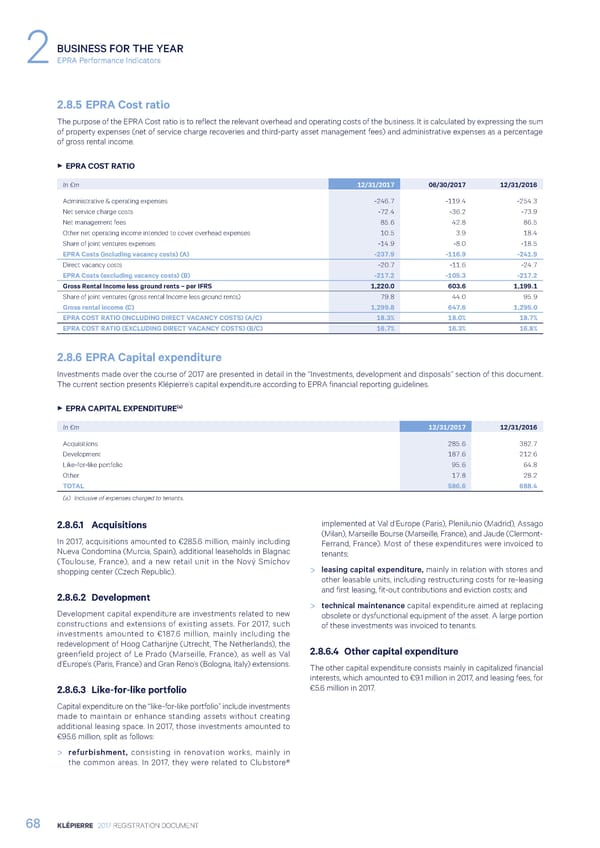

BUSINESS FOR THE YEAR 2EPRA Performance Indicators 2.8.5 EPRA Cost ratio The purpose of the EPRA Cost ratio is to reflect the relevant overhead and operating costs of the business. It is calculated by expressing the sum of property expenses (net of service charge recoveries and third-party asset management fees) and administrative expenses as a percentage of gross rental income. 3 EPRA COST RATIO In €m 12/31/2017 06/30/2017 12/31/2016 Administrative & operating expenses -246.7 -119.4 -254.3 Net service charge costs -72.4 -36.2 -73.9 Net management fees 85.6 42.8 86.5 Other net operating income intended to cover overhead expenses 10.5 3.9 18.4 Share of joint ventures expenses -14.9 -8.0 -18.5 EPRA Costs (including vacancy costs) (A) -237.9 -116.9 -241.9 Direct vacancy costs -20.7 -11.6 -24.7 EPRA Costs (excluding vacancy costs) (B) -217.2 -105.3 -217.2 Gross Rental Income less ground rents – per IFRS 1,220.0 603.6 1,199.1 Share of joint ventures (gross rental Income less ground rents) 79.8 44.0 95.9 Gross rental income (C) 1,299.8 647.6 1,295.0 EPRA COST RATIO (INCLUDING DIRECT VACANCY COSTS) (A/C) 18.3% 18.0% 18.7% EPRA COST RATIO (EXCLUDING DIRECT VACANCY COSTS) (B/C) 16.7% 16.3% 16.8% 2.8.6 EPRA Capital expenditure Investments made over the course of 2017 are presented in detail in the “Investments, development and disposals” section of this document. The current section presents Klépierre’s capital expenditure according to EPRA financial reporting guidelines. 3 EPRA CAPITAL EXPENDITURE(a) In €m 12/31/2017 12/31/2016 Acquisitions 285.6 382.7 Development 187.6 212.6 Like-for-like portfolio 95.6 64.8 Other 17.8 28.2 TOTAL 586.6 688.4 (a) Inclusive of expenses charged to tenants. 2.8.6.1 Acquisitions implemented at Val d’Europe (Paris), Plenilunio (Madrid), Assago (Milan), Marseille Bourse (Marseille, France), and Jaude (Clermont- In 2017, acquisitions amounted to €285.6 million, mainly including Ferrand, France). Most of these expenditures were invoiced to Nueva Condomina (Murcia, Spain), additional leaseholds in Blagnac tenants; (Toulouse, France), and a new retail unit in the Nový Smíchov shopping center (Czech Republic). > leasing capital expenditure, mainly in relation with stores and other leasable units, including restructuring costs for re-leasing 2.8.6.2 Development and first leasing, fit-out contributions and eviction costs; and > technical maintenance capital expenditure aimed at replacing Development capital expenditure are investments related to new obsolete or dysfunctional equipment of the asset. A large portion constructions and extensions of existing assets. For 2017, such of these investments was invoiced to tenants. investments amounted to €187.6 million, mainly including the redevelopment of Hoog Catharijne (Utrecht, The Netherlands), the 2.8.6.4 Other capital expenditure greenfield project of Le Prado (Marseille, France), as well as Val d’Europe’s (Paris, France) and Gran Reno’s (Bologna, Italy) extensions. The other capital expenditure consists mainly in capitalized financial interests, which amounted to €9.1 million in 2017, and leasing fees, for 2.8.6.3 Like-for-like portfolio €5.6 million in 2017. Capital expenditure on the “like-for-like portfolio” include investments made to maintain or enhance standing assets without creating additional leasing space. In 2017, those investments amounted to €95.6 million, split as follows: > refurbishment, consisting in renovation works, mainly in the common areas. In 2017, they were related to Clubstore® 68 KLÉPIERRE 2017 REGISTRATION DOCUMENT

Registration Document 2017 Page 69 Page 71

Registration Document 2017 Page 69 Page 71