.png)

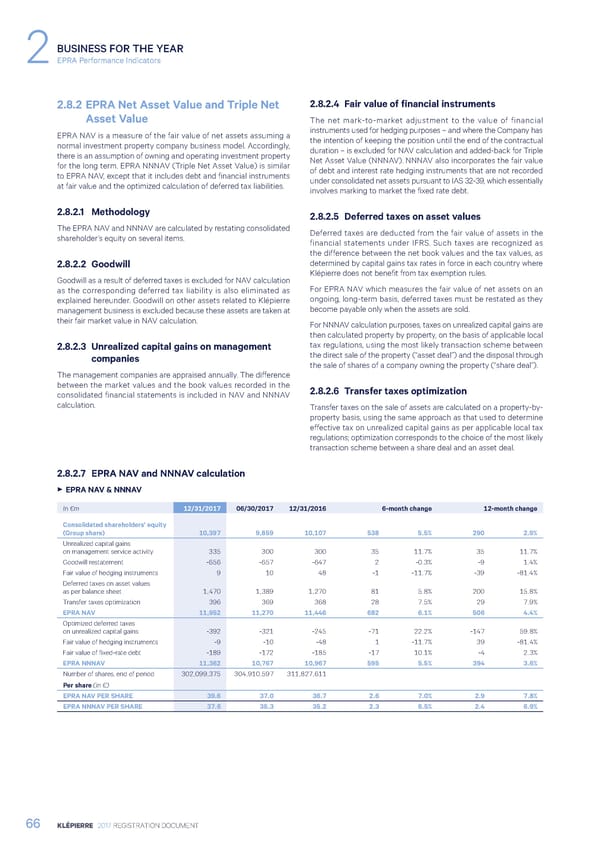

BUSINESS FOR THE YEAR 2EPRA Performance Indicators 2.8.2 EPRA Net Asset Value and Triple Net 2.8.2.4 Fair value of financial instruments Asset Value The net mark-to-market adjustment to the value of financial EPRA NAV is a measure of the fair value of net assets assuming a instruments used for hedging purposes – and where the Company has normal investment property company business model. Accordingly, the intention of keeping the position until the end of the contractual there is an assumption of owning and operating investment property duration – is excluded for NAV calculation and added-back for Triple for the long term. EPRA NNNAV (Triple Net Asset Value) is similar Net Asset Value (NNNAV). NNNAV also incorporates the fair value to EPRA NAV, except that it includes debt and financial instruments of debt and interest rate hedging instruments that are not recorded at fair value and the optimized calculation of deferred tax liabilities. under consolidated net assets pursuant to IAS 32-39, which essentially involves marking to market the fixed rate debt. 2.8.2.1 Methodology 2.8.2.5 Deferred taxes on asset values The EPRA NAV and NNNAV are calculated by restating consolidated Deferred taxes are deducted from the fair value of assets in the shareholder’s equity on several items. financial statements under IFRS. Such taxes are recognized as the difference between the net book values and the tax values, as 2.8.2.2 Goodwill determined by capital gains tax rates in force in each country where Goodwill as a result of deferred taxes is excluded for NAV calculation Klépierre does not benefit from tax exemption rules. as the corresponding deferred tax liability is also eliminated as For EPRA NAV which measures the fair value of net assets on an explained hereunder. Goodwill on other assets related to Klépierre ongoing, long-term basis, deferred taxes must be restated as they management business is excluded because these assets are taken at become payable only when the assets are sold. their fair market value in NAV calculation. For NNNAV calculation purposes, taxes on unrealized capital gains are then calculated property by property, on the basis of applicable local 2.8.2.3 Unrealized capital gains on management tax regulations, using the most likely transaction scheme between companies the direct sale of the property (“asset deal”) and the disposal through the sale of shares of a company owning the property (“share deal”). The management companies are appraised annually. The difference between the market values and the book values recorded in the 2.8.2.6 Transfer taxes optimization consolidated financial statements is included in NAV and NNNAV calculation. Transfer taxes on the sale of assets are calculated on a property-by- property basis, using the same approach as that used to determine effective tax on unrealized capital gains as per applicable local tax regulations; optimization corresponds to the choice of the most likely transaction scheme between a share deal and an asset deal. 2.8.2.7 EPRA NAV and NNNAV calculation 3 EPRA NAV & NNNAV In €m 12/31/2017 06/30/2017 12/31/2016 6-month change 12-month change Consolidated shareholders’ equity (Group share) 10,397 9,859 10,107 538 5.5% 290 2.9% Unrealized capital gains on management service activity 335 300 300 35 11.7% 35 11.7% Goodwill restatement -656 -657 -647 2 -0.3% -9 1.4% Fair value of hedging instruments 9 10 48 -1 -11.7% -39 -81.4% Deferred taxes on asset values as per balance sheet 1,470 1,389 1,270 81 5.8% 200 15.8% Transfer taxes optimization 396 369 368 28 7.5% 29 7.9% EPRA NAV 11,952 11,270 11,446 682 6.1% 506 4.4% Optimized deferred taxes on unrealized capital gains -392 -321 -245 -71 22.2% -147 59.8% Fair value of hedging instruments -9 -10 -48 1 -11.7% 39 -81.4% Fair value of fixed-rate debt -189 -172 -185 -17 10.1% -4 2.3% EPRA NNNAV 11,362 10,767 10,967 595 5.5% 394 3.6% Number of shares, end of period 302,099,375 304,910,597 311,827,611 Per share (in €) EPRA NAV PER SHARE 39.6 37.0 36.7 2.6 7.0% 2.9 7.8% EPRA NNNAV PER SHARE 37.6 35.3 35.2 2.3 6.5% 2.4 6.9% 66 KLÉPIERRE 2017 REGISTRATION DOCUMENT

Registration Document 2017 Page 67 Page 69

Registration Document 2017 Page 67 Page 69