.png)

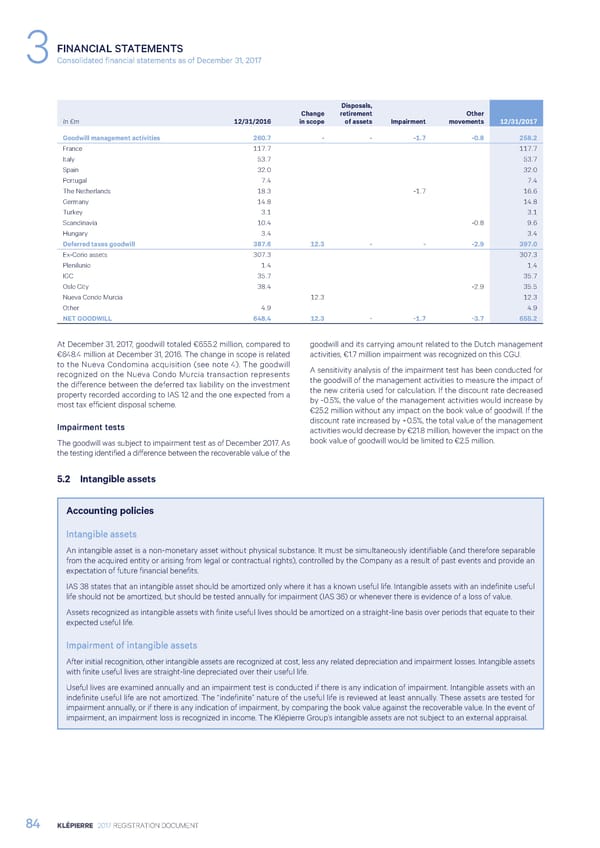

FINANCIAL STATEMENTS 3Consolidated financial statements as of December 31, 2017 Disposals, Change retirement Other In €m 12/31/2016 in scope of assets Impairment movements 12/31/2017 Goodwill management activities 260.7 - - -1.7 -0.8 258.2 France 117.7 117.7 Italy 53.7 53.7 Spain 32.0 32.0 Portugal 7.4 7.4 The Netherlands 18.3 -1.7 16.6 Germany 14.8 14.8 Turkey 3.1 3.1 Scandinavia 10.4 -0.8 9.6 Hungary 3.4 3.4 Deferred taxes goodwill 387.6 12.3 - - -2.9 397.0 Ex-Corio assets 307.3 307.3 Plenilunio 1.4 1.4 IGC 35.7 35.7 Oslo City 38.4 -2.9 35.5 Nueva Condo Murcia 12.3 12.3 Other 4.9 4.9 NET GOODWILL 648.4 12.3 - -1.7 -3.7 655.2 At December 31, 2017, goodwill totaled €655.2 million, compared to goodwill and its carrying amount related to the Dutch management €648.4 million at December 31, 2016. The change in scope is related activities, €1.7 million impairment was recognized on this CGU. to the Nueva Condomina acquisition (see note 4). The goodwill A sensitivity analysis of the impairment test has been conducted for recognized on the Nueva Condo Murcia transaction represents the goodwill of the management activities to measure the impact of the difference between the deferred tax liability on the investment the new criteria used for calculation. If the discount rate decreased property recorded according to IAS 12 and the one expected from a by -0.5%, the value of the management activities would increase by most tax efficient disposal scheme. €25.2 million without any impact on the book value of goodwill. If the Impairment tests discount rate increased by +0.5%, the total value of the management activities would decrease by €21.8 million, however the impact on the The goodwill was subject to impairment test as of December 2017. As book value of goodwill would be limited to €2.5 million. the testing identified a difference between the recoverable value of the 5.2 Intangible assets Accounting policies Intangible assets An intangible asset is a non-monetary asset without physical substance. It must be simultaneously identifiable (and therefore separable from the acquired entity or arising from legal or contractual rights), controlled by the Company as a result of past events and provide an expectation of future financial benefits. IAS 38 states that an intangible asset should be amortized only where it has a known useful life. Intangible assets with an indefinite useful life should not be amortized, but should be tested annually for impairment (IAS 36) or whenever there is evidence of a loss of value. Assets recognized as intangible assets with finite useful lives should be amortized on a straight-line basis over periods that equate to their expected useful life. Impairment of intangible assets After initial recognition, other intangible assets are recognized at cost, less any related depreciation and impairment losses. Intangible assets with finite useful lives are straight-line depreciated over their useful life. Useful lives are examined annually and an impairment test is conducted if there is any indication of impairment. Intangible assets with an indefinite useful life are not amortized. The “indefinite” nature of the useful life is reviewed at least annually. These assets are tested for impairment annually, or if there is any indication of impairment, by comparing the book value against the recoverable value. In the event of impairment, an impairment loss is recognized in income. The Klépierre Group’s intangible assets are not subject to an external appraisal. 84 KLÉPIERRE 2017 REGISTRATION DOCUMENT

Registration Document 2017 Page 85 Page 87

Registration Document 2017 Page 85 Page 87