.png)

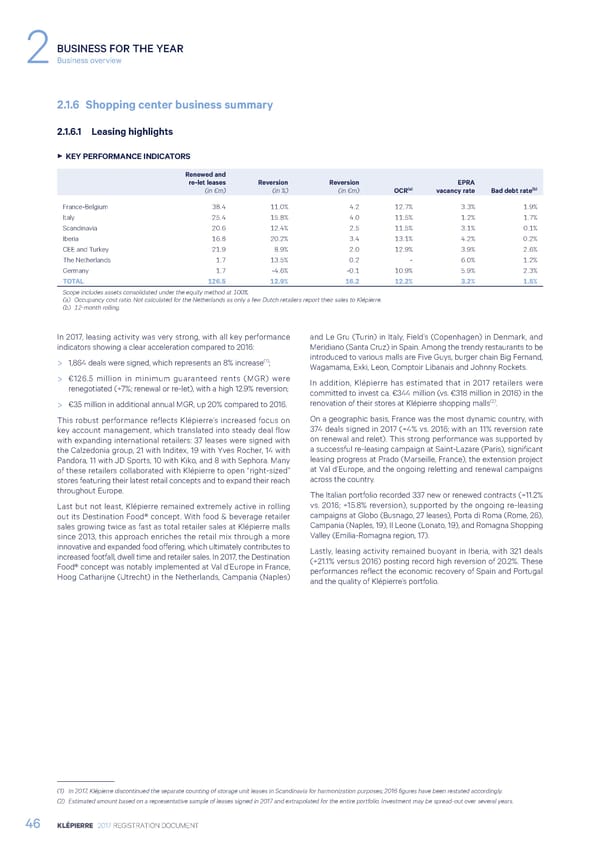

BUSINESS FOR THE YEAR 2Business overview 2.1.6 Shopping center business summary 2.1.6.1 Leasing highlights 3 KEY PERFORMANCE INDICATORS Renewed and re-let leases Reversion Reversion EPRA (a) (b) (in €m) (in %) (in €m) OCR vacancy rate Bad debt rate France-Belgium 38.4 11.0% 4.2 12.7% 3.3% 1.9% Italy 25.4 15.8% 4.0 11.5% 1.2% 1.7% Scandinavia 20.6 12.4% 2.5 11.5% 3.1% 0.1% Iberia 16.8 20.2% 3.4 13.1% 4.2% 0.2% CEE and Turkey 21.9 8.9% 2.0 12.9% 3.9% 2.6% The Netherlands 1.7 13.5% 0.2 - 6.0% 1.2% Germany 1.7 -4.6% -0.1 10.9% 5.9% 2.3% TOTAL 126.5 12.9% 16.2 12.2% 3.2% 1.5% Scope includes assets consolidated under the equity method at 100%. (a) Occupancy cost ratio. Not calculated for the Netherlands as only a few Dutch retailers report their sales to Klépierre. (b) 12-month rolling. In 2017, leasing activity was very strong, with all key performance and Le Gru (Turin) in Italy, Field’s (Copenhagen) in Denmark, and indicators showing a clear acceleration compared to 2016: Meridiano (Santa Cruz) in Spain. Among the trendy restaurants to be (1) introduced to various malls are Five Guys, burger chain Big Fernand, > 1,864 deals were signed, which represents an 8% increase ; Wagamama, Exki, Leon, Comptoir Libanais and Johnny Rockets. > €126.5 million in minimum guaranteed rents (MGR) were In addition, Klépierre has estimated that in 2017 retailers were renegotiated (+7%; renewal or re-let), with a high 12.9% reversion; committed to invest ca. €344 million (vs. €318 million in 2016) in the (2) > €35 million in additional annual MGR, up 20% compared to 2016. renovation of their stores at Klépierre shopping malls . This robust performance reflects Klépierre’s increased focus on On a geographic basis, France was the most dynamic country, with key account management, which translated into steady deal flow 374 deals signed in 2017 (+4% vs. 2016; with an 11% reversion rate with expanding international retailers: 37 leases were signed with on renewal and relet). This strong performance was supported by the Calzedonia group, 21 with Inditex, 19 with Yves Rocher, 14 with a successful re-leasing campaign at Saint-Lazare (Paris), significant Pandora, 11 with JD Sports, 10 with Kiko, and 8 with Sephora. Many leasing progress at Prado (Marseille, France), the extension project of these retailers collaborated with Klépierre to open “right-sized” at Val d’Europe, and the ongoing reletting and renewal campaigns stores featuring their latest retail concepts and to expand their reach across the country. throughout Europe. The Italian portfolio recorded 337 new or renewed contracts (+11.2% Last but not least, Klépierre remained extremely active in rolling vs. 2016; +15.8% reversion), supported by the ongoing re-leasing out its Destination Food® concept. With food & beverage retailer campaigns at Globo (Busnago, 27 leases), Porta di Roma (Rome, 26), sales growing twice as fast as total retailer sales at Klépierre malls Campania (Naples, 19), Il Leone (Lonato, 19), and Romagna Shopping since 2013, this approach enriches the retail mix through a more Valley (Emilia-Romagna region, 17). innovative and expanded food offering, which ultimately contributes to Lastly, leasing activity remained buoyant in Iberia, with 321 deals increased footfall, dwell time and retailer sales. In 2017, the Destination (+21.1% versus 2016) posting record high reversion of 20.2%. These Food® concept was notably implemented at Val d’Europe in France, performances reflect the economic recovery of Spain and Portugal Hoog Catharijne (Utrecht) in the Netherlands, Campania (Naples) and the quality of Klépierre’s portfolio. (1) In 2017, Klépierre discontinued the separate counting of storage unit leases in Scandinavia for harmonization purposes; 2016 figures have been restated accordingly. (2) Estimated amount based on a representative sample of leases signed in 2017 and extrapolated for the entire portfolio. Investment may be spread-out over several years. 46 KLÉPIERRE 2017 REGISTRATION DOCUMENT

Registration Document 2017 Page 47 Page 49

Registration Document 2017 Page 47 Page 49