.png)

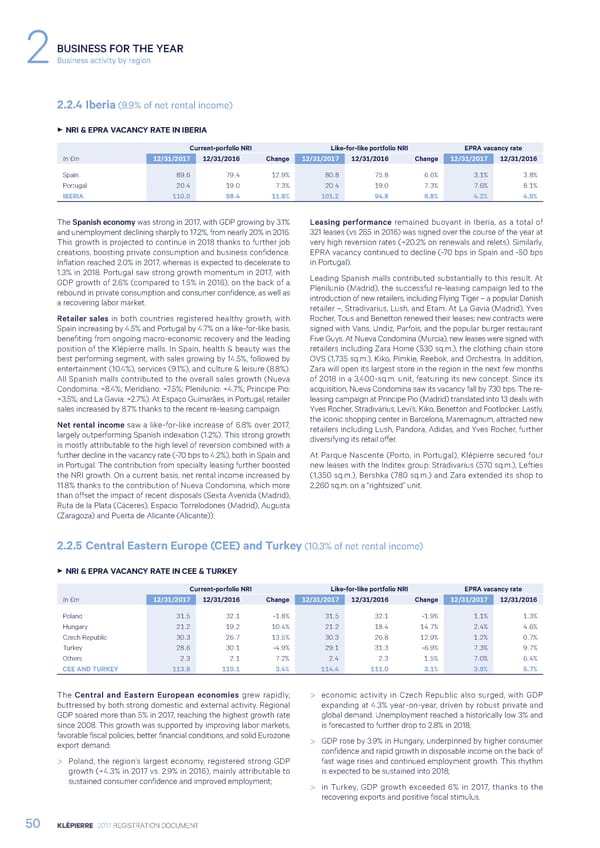

BUSINESS FOR THE YEAR 2Business activity by region 2.2.4 Iberia (9.9% of net rental income) 3 NRI & EPRA VACANCY RATE IN IBERIA Current-porfolio NRI Like-for-like portfolio NRI EPRA vacancy rate In €m 12/31/2017 12/31/2016 Change 12/31/2017 12/31/2016 Change 12/31/2017 12/31/2016 Spain 89.6 79.4 12.9% 80.8 75.8 6.6% 3.1% 3.8% Portugal 20.4 19.0 7.3% 20.4 19.0 7.3% 7.6% 8.1% IBERIA 110.0 98.4 11.8% 101.2 94.8 6.8% 4.2% 4.9% The Spanish economy was strong in 2017, with GDP growing by 3.1% Leasing performance remained buoyant in Iberia, as a total of and unemployment declining sharply to 17.2%, from nearly 20% in 2016. 321 leases (vs 265 in 2016) was signed over the course of the year at This growth is projected to continue in 2018 thanks to further job very high reversion rates (+20.2% on renewals and relets). Similarly, creations, boosting private consumption and business confidence. EPRA vacancy continued to decline (-70 bps in Spain and -50 bps Inflation reached 2.0% in 2017, whereas is expected to decelerate to in Portugal). 1.3% in 2018. Portugal saw strong growth momentum in 2017, with Leading Spanish malls contributed substantially to this result. At GDP growth of 2.6% (compared to 1.5% in 2016), on the back of a Plenilunio (Madrid), the successful re-leasing campaign led to the rebound in private consumption and consumer confidence, as well as introduction of new retailers, including Flying Tiger – a popular Danish a recovering labor market. retailer –, Stradivarius, Lush, and Etam. At La Gavia (Madrid), Yves Retailer sales in both countries registered healthy growth, with Rocher, Tous and Benetton renewed their leases; new contracts were Spain increasing by 4.5% and Portugal by 4.7% on a like-for-like basis, signed with Vans, Undiz, Parfois, and the popular burger restaurant benefiting from ongoing macro-economic recovery and the leading Five Guys. At Nueva Condomina (Murcia), new leases were signed with position of the Klépierre malls. In Spain, health & beauty was the retailers including Zara Home (530 sq.m.), the clothing chain store best performing segment, with sales growing by 14.5%, followed by OVS (1,735 sq.m.), Kiko, Pimkie, Reebok, and Orchestra. In addition, entertainment (10.4%), services (9.1%), and culture & leisure (8.8%). Zara will open its largest store in the region in the next few months All Spanish malls contributed to the overall sales growth (Nueva of 2018 in a 3,400-sq.m. unit, featuring its new concept. Since its Condomina: +8.4%; Meridiano: +7.5%; Plenilunio: +4.7%; Principe Pio: acquisition, Nueva Condomina saw its vacancy fall by 730 bps. The re- +3.5%; and La Gavia: +2.7%). At Espaço Guimarães, in Portugal, retailer leasing campaign at Principe Pio (Madrid) translated into 13 deals with sales increased by 8.7% thanks to the recent re-leasing campaign. Yves Rocher, Stradivarius, Levi’s, Kiko, Benetton and Footlocker. Lastly, Net rental income saw a like-for-like increase of 6.8% over 2017, the iconic shopping center in Barcelona, Maremagnum, attracted new largely outperforming Spanish indexation (1.2%). This strong growth retailers including Lush, Pandora, Adidas, and Yves Rocher, further is mostly attributable to the high level of reversion combined with a diversifying its retail offer. further decline in the vacancy rate (-70 bps to 4.2%), both in Spain and At Parque Nascente (Porto, in Portugal), Klépierre secured four in Portugal. The contribution from specialty leasing further boosted new leases with the Inditex group: Stradivarius (570 sq.m.), Lefties the NRI growth. On a current basis, net rental income increased by (1,350 sq.m.), Bershka (780 sq.m.) and Zara extended its shop to 11.8% thanks to the contribution of Nueva Condomina, which more 2,260 sq.m. on a “rightsized” unit. than offset the impact of recent disposals (Sexta Avenida (Madrid), Ruta de la Plata (Cáceres), Espacio Torrelodones (Madrid), Augusta (Zaragoza) and Puerta de Alicante (Alicante)). 2.2.5 Central Eastern Europe (CEE) and Turkey (10.3% of net rental income) 3 NRI & EPRA VACANCY RATE IN CEE & TURKEY Current-porfolio NRI Like-for-like portfolio NRI EPRA vacancy rate In €m 12/31/2017 12/31/2016 Change 12/31/2017 12/31/2016 Change 12/31/2017 12/31/2016 Poland 31.5 32.1 -1.8% 31.5 32.1 -1.9% 1.1% 1.3% Hungary 21.2 19.2 10.4% 21.2 18.4 14.7% 2.4% 4.6% Czech Republic 30.3 26.7 13.5% 30.3 26.8 12.9% 1.2% 0.7% Turkey 28.6 30.1 -4.9% 29.1 31.3 -6.9% 7.3% 9.7% Others 2.3 2.1 7.2% 2.4 2.3 1.5% 7.0% 6.4% CEE AND TURKEY 113.8 110.1 3.4% 114.4 111.0 3.1% 3.9% 5.7% The Central and Eastern European economies grew rapidly, > economic activity in Czech Republic also surged, with GDP buttressed by both strong domestic and external activity. Regional expanding at 4.3% year-on-year, driven by robust private and GDP soared more than 5% in 2017, reaching the highest growth rate global demand. Unemployment reached a historically low 3% and since 2008. This growth was supported by improving labor markets, is forecasted to further drop to 2.8% in 2018; favorable fiscal policies, better financial conditions, and solid Eurozone > GDP rose by 3.9% in Hungary, underpinned by higher consumer export demand: confidence and rapid growth in disposable income on the back of > Poland, the region’s largest economy, registered strong GDP fast wage rises and continued employment growth. This rhythm growth (+4.3% in 2017 vs. 2.9% in 2016), mainly attributable to is expected to be sustained into 2018; sustained consumer confidence and improved employment; > in Turkey, GDP growth exceeded 6% in 2017, thanks to the recovering exports and positive fiscal stimulus. 50 KLÉPIERRE 2017 REGISTRATION DOCUMENT

Registration Document 2017 Page 51 Page 53

Registration Document 2017 Page 51 Page 53