.png)

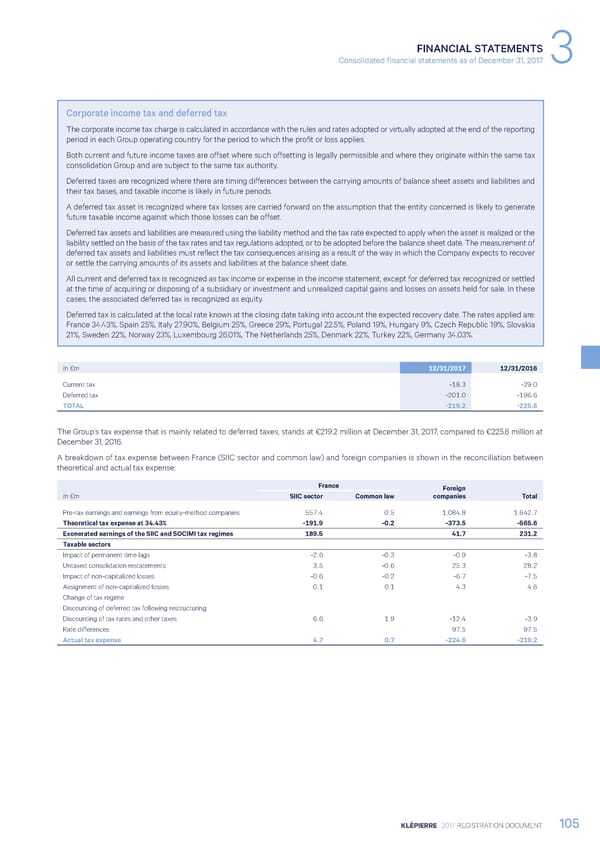

FINANCIAL STATEMENTS Consolidated financial statements as of December 31, 2017 3 Corporate income tax and deferred tax The corporate income tax charge is calculated in accordance with the rules and rates adopted or virtually adopted at the end of the reporting period in each Group operating country for the period to which the profit or loss applies. Both current and future income taxes are offset where such offsetting is legally permissible and where they originate within the same tax consolidation Group and are subject to the same tax authority. Deferred taxes are recognized where there are timing differences between the carrying amounts of balance sheet assets and liabilities and their tax bases, and taxable income is likely in future periods. A deferred tax asset is recognized where tax losses are carried forward on the assumption that the entity concerned is likely to generate future taxable income against which those losses can be offset. Deferred tax assets and liabilities are measured using the liability method and the tax rate expected to apply when the asset is realized or the liability settled on the basis of the tax rates and tax regulations adopted, or to be adopted before the balance sheet date. The measurement of deferred tax assets and liabilities must reflect the tax consequences arising as a result of the way in which the Company expects to recover or settle the carrying amounts of its assets and liabilities at the balance sheet date. All current and deferred tax is recognized as tax income or expense in the income statement, except for deferred tax recognized or settled at the time of acquiring or disposing of a subsidiary or investment and unrealized capital gains and losses on assets held for sale. In these cases, the associated deferred tax is recognized as equity. Deferred tax is calculated at the local rate known at the closing date taking into account the expected recovery date. The rates applied are: France 34.43%, Spain 25%, Italy 27.90%, Belgium 25%, Greece 29%, Portugal 22.5%, Poland 19%, Hungary 9%, Czech Republic 19%, Slovakia 21%, Sweden 22%, Norway 23%, Luxembourg 26.01%, The Netherlands 25%, Denmark 22%, Turkey 22%, Germany 34.03%. In €m 12/31/2017 12/31/2016 Current tax -18.3 -29.0 Deferred tax -201.0 -196.6 TOTAL -219.2 -225.6 The Group’s tax expense that is mainly related to deferred taxes, stands at €219.2 million at December 31, 2017, compared to €225.6 million at December 31, 2016. A breakdown of tax expense between France (SIIC sector and common law) and foreign companies is shown in the reconciliation between theoretical and actual tax expense: France Foreign In €m SIIC sector Common law companies Total Pre-tax earnings and earnings from equity-method companies 557.4 0.5 1,084.8 1,642.7 Theoretical tax expense at 34.43% -191.9 -0.2 -373.5 -565.6 Exonerated earnings of the SIIC and SOCIMI tax regimes 189.5 41.7 231.2 Taxable sectors Impact of permanent time lags -2.6 -0.3 -0.9 -3.8 Untaxed consolidation restatements 3.5 -0.6 25.3 28.2 Impact of non-capitalized losses -0.6 -0.2 -6.7 -7.5 Assignment of non-capitalized losses 0.1 0.1 4.3 4.6 Change of tax regime Discounting of deferred tax following restructuring Discounting of tax rates and other taxes 6.6 1.9 -12.4 -3.9 Rate differences 97.5 97.5 Actual tax expense 4.7 0.7 -224.6 -219.2 KLÉPIERRE 2017 REGISTRATION DOCUMENT 105

Registration Document 2017 Page 106 Page 108

Registration Document 2017 Page 106 Page 108